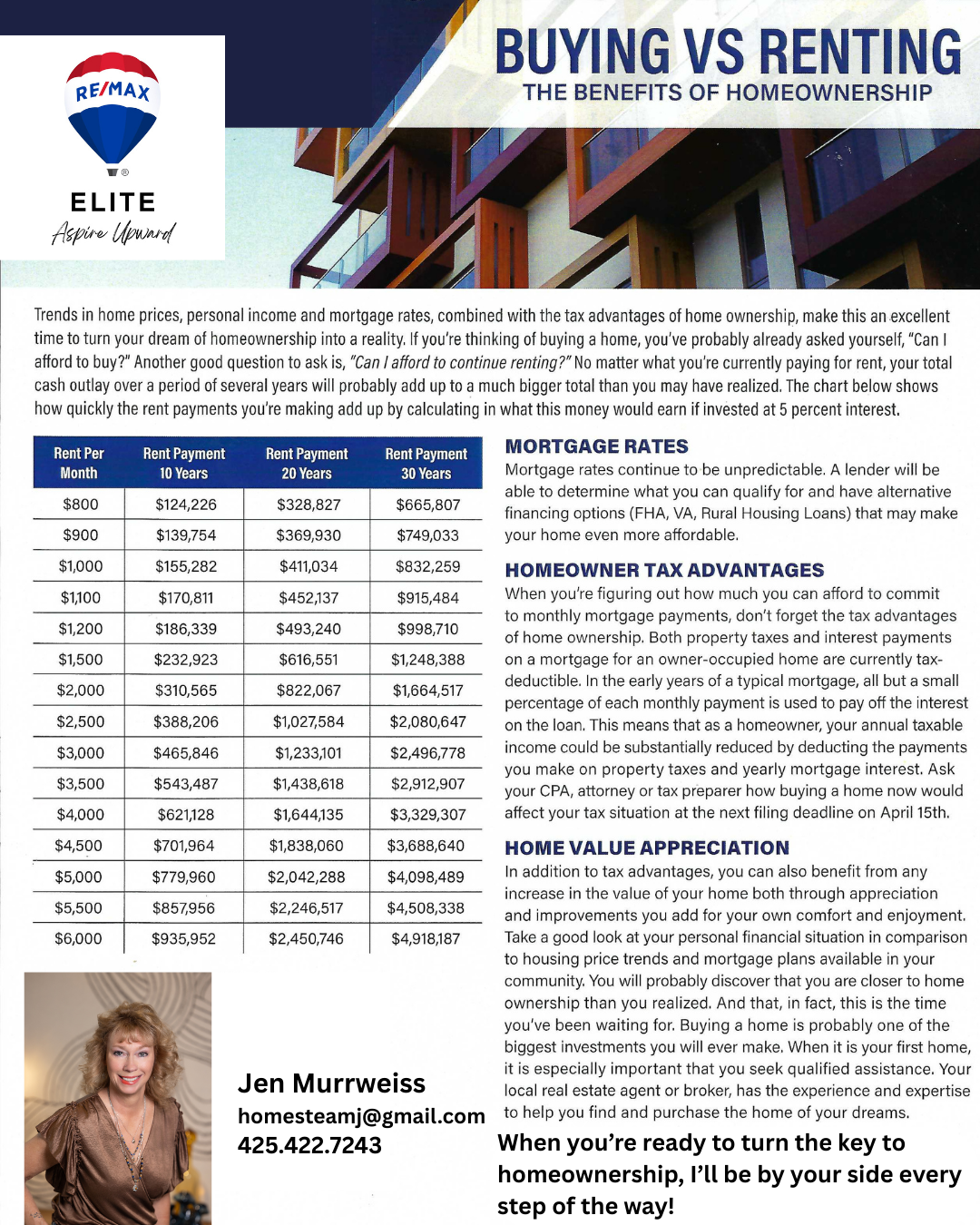

BUYING VS. RENTING

Happy September, friends! 🍂 This month’s newsletter is packed with:

📊 A fresh Eye on the Market

🏡 Fall home décor ideas to cozy up your space

📦 Clever space-saving tips

🎶 Can’t-miss local events around the Sound Grab your coffee ☕ and take a few minutes to check it out—you’ll love what’s inside! 💌

🎉✨ Happy New Year! 🎉✨

Welcome to 2025! 🏡 Whether you’re looking to dive into the real estate market, stay in the loop with the latest events, or pick up some fresh tips & tricks, this month’s newsletter has it all! 🌟 Get ready to kick off the year with exciting opportunities, expert insights, and a little inspiration to make 2025 your best year yet! 💪🔑 Let’s jump right in!

🌷🏡 Welcome to March!! As spring blooms around us, so does the real estate market! 🌱🏠 With the promise of warmer days ahead, it’s the perfect time to explore new listings and envision your dream home. 🌞💭 Keep an eye out for my market updates and expert tips to help you navigate the buying or selling process with ease. Plus, don’t miss out on exciting local events popping up across the county and beyond – because life’s too short to miss out on community fun! 🎉🌳 Let’s make March a month of new beginnings and exciting possibilities in the world of real estate! 🌟 🏘️✨

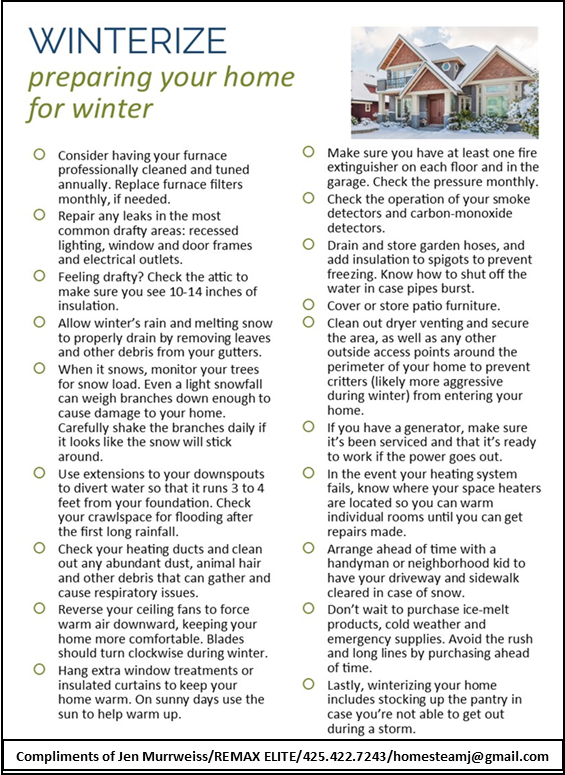

🌬️❄️ Winter is upon us, and while the season brings a magical snowscape, it also brings the risk of burst pipes, frozen woes, and unexpected home headaches! Don’t let the chill catch you off guard—warm up with these reminders on prepping your home for winter! 🏡✨

Because when it comes to your home, it’s better to be prepared than to face a chilly surprise! 🧤🔥 #WinterReadyHome #HomeSweetWarmHome

Getting preapproved before you start looking at homes is crucial for several reasons:

In summary, getting preapproved is a strategic step that not only gives you a clear financial picture but also positions you as a serious buyer in the real estate market. It enhances your ability to make informed decisions and increases your chances of securing the home you desire. If you are in the Puget Sound region reach out to me and I will guide you to the best lender associates based on you needs and we will work together to get you the perfect home that goes together beautfully. Just like peanut butter and jelly!

When retirement looms, financial stability is a gnawing concern for most people. Have I saved enough? What will inflation do to my nest egg? Will Social Security remain solvent? What are the health wildcards I haven’t planned for? As such, it’s wise to slash expenses and debt as much as possible, with the idea of entering retirement debt-free. For some, that means paying off the mortgage by accelerating their mortgage payoff.

Experian (https://bit.ly/3srAgU7) found that the average mortgage balance debt by generation in 2022 was:

Generation X (age 42-57): $274,406| Baby Boomers (58-76): $189,155 | Silent Generation (77+): $139,999

If you’re able to afford to put extra cash toward your mortgage, doing an early payoff can be a powerful strategy that not only cuts interest payments but lightens the financial and emotional load during retirement, bringing peace of mind, more money for hobbies, vacations, and funds for healthcare and long-term care expenses.

Still, before deciding, you must take a complete look at your financial picture to be sure that a faster payoff is the best way to achieve your goals and to understand the potential sacrifices and downsides of such a move.

Here are nine considerations.

1. Understand the risks. If you have a relatively low mortgage rate, could you miss out on higher returns on your money by putting the extra toward your mortgage? Will you miss out on mortgage interest deductions? By devoting money to your mortgage, you’re lowering your liquidity. Will that lack of liquidity adversely affect your other long-term goals or short-term needs? For example, are you hoping to give a chunk of money to help a child with a down payment or planning to pay some of your grandchild’s college costs?

2. Examine your debts. If you have credit cards, personal loans, and other obligations, paying those off is better before accelerating your mortgage payments. First, pay off debts with higher interest rates than your current mortgage because consumer debt typically carries higher interest rates than mortgages.

3. Understand your mortgage agreement. Read your agreement’s fine print and talk to your lender to be sure there aren’t prepayment penalties and that you’re allowed to make extra payments.

4. Calculate your savings. How quickly do you want to pay off your mortgage? Can you afford to shave five years or ten years off your mortgage? Use an online mortgage calculator to see how much principal you must pay every month or year to pay off a loan in a certain number of years and how much you’ll save with an early payoff. The savings can be significant. According to a NerdWallet calculator (https://bit.ly/45MhzZR), for example, if you took out a $300,000 30-year fixed loan at 5.5%, have ten years left, and decide to pay it off in five years, you’d have to pay an extra $206.75 monthly. The move would save $89,796.84 over the life of the loan.

5. Develop your repayment plan. Will you make an annual lump-sum payment or extra payments monthly or bi-weekly? One advantage of spreading the additional payments across the year and making bi-weekly payments is that you lower your principal balance each month, creating a smaller balance on which interest is calculated.

6. Look at your budget. How much extra money can you afford to put toward your mortgage? Where can you cut back? Also, consider the sacrifices you’ll need to make and decide if missing out on a vacation or cutting back on hobbies is worth it.

7. Don’t sacrifice retirement savings. Have an adequate emergency fund before shifting money to speed up your mortgage payoff. Also, be sure you’ll still be able to max out all your retirement vehicles like 401ks, Roth IRAs, and Health Savings Accounts and make catch-up contributions.

8. Pay the right way. Be sure to tell your mortgage holder that your extra payments will be applied to the loan principal, not the next month’s mortgage payment.

9. Talk to experts. Remember that there’s no one-size-fits-all approach with finances, so get advice from financial pros—your accountant and financial planner, for example—to understand the risks and the impact an early mortgage payoff would have on your other goals.

Autumn Adventures Await!

As the leaves start to turn brilliant shades of red and gold, and a crispness fills the air, it’s clear that autumn has arrived! Welcome to October and your newsletter with your eye on the market, a few home tips/tricks PLUS this delightful season comes with a cornucopia of local fall and Halloween activities that are sure to enchant and thrill. So, grab your cozy sweaters and pumpkin spice lattes, because we’ve rounded up some of the most exciting events happening right in our area!

| Check Out These Fall Events: | |

| The Harvest at Skagit Acres | |

| Fife Harvest Festival | |

| Seattle Chocolate Haunted Factory Tour | |

| Stalker Farms | |

| Serres Farm Pumpkin Patch | |

| Cider Fest | |

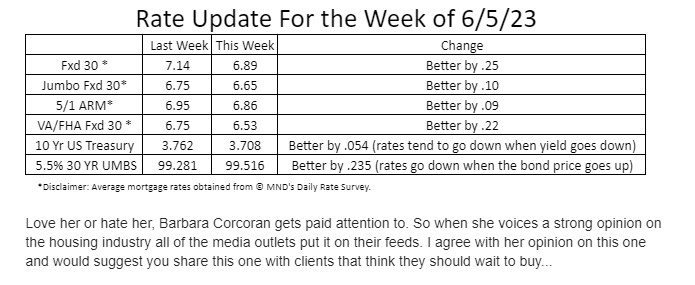

Self-made real estate millionaire Barbara Corcoran says it’s a ‘good time to buy’ because home prices are going to ‘explode’ when mortgage rates drop!

Alena Botros

Fri, June 2, 2023 at 2:00 AM PDT·4 min read

Appearing as a guest on Good Morning America this week, Barbara Corcoran answered several questions from viewers, ranging from when the right time to buy a home is to how to win a bidding war. As for the former, Corcoran said now is the time to buy.

“It’s a good time to buy because the minute interest rates go down, everybody’s waiting for them to go down even by a point, and when they do, they’re going to come rushing back in the market,” Corcoran said. “Prices are going to explode, and you’re going to be paying more for the same house. And you can always refinance, remember, when and if interest rates come down.”

It’s not Corcoran’s first time advising against even attempting to time the market. Previously, on the Chicks in the Office podcast, Corcoran said to forget about the timing, again stressing that now is always the time to buy.

The self-proclaimed “NYC Real Estate Queen,” founded the Corcoran Group with a $1,000 loan in 1973, which she famously turned into $66 million, after selling her business in 2001. She’ll always be a powerhouse within the real estate industry, but now most people know her as the spunky, blunt, and well-dressed shark on ABC’s Shark Tank.

Another viewer asked Corcoran how to win bidding wars, saying that he and his fiancee have been looking for a house but have been out bid every time they’ve found one they like. Corcoran said the key is to look like the “best deal in town,” while playing on the seller’s emotions.

“You have to be prequalified for your mortgage so you can go in there as an all cash deal. I’m an all cash deal, it’s not contingent, I already got my mortgage—you want that power behind you,” Corcoran said. “You also want to go in and realize it’s never just a financial deal. Get a nice piece of stationery and handwrite a note to that owner, and tell them how much you love the house. It makes a difference because people like to sell homes to people who love their house.”

As for the different types of mortgage loans that buyers can choose from, Corcoran said it depends on how long you’re going to live in that home. If you’re going to live there a long time, or at least except you are, Corcoran said a conventional rate mortgage at the shortest term you can afford, is the best option. On the other hand, if you’re only going to be living there for a short period of time, likely under five years, she said you’ll want to get an adjustable rate mortgage because it’s cheaper.

When Corcoran was then asked if there’s any way to get relief as someone who’s “house poor,” a term used to describe someone that’s spending more than 30% of their income on housing, she answered: “you don’t get relief from that.” In coastal cities, Corcoran said, people are spending more than 40% of their income on housing. But there’s a light at the end of the tunnel, in her view—people are forced to save by paying off their mortgage.

“When it comes time to retire, for most of us, it’s the only money we have to retire on,” Corcoran said.

Now if you want to make the most out of your home purchase, she said you’ll always get the best return in a high-traffic area. And if you want to make a killing, buy a home in an up and coming area. Corcoran’s formula for doing so? Follow the creative community and see where they’re living, and check out the nightlife.

And of course, a Corcoran Q&A couldn’t be complete without touching on rentals and renting. As for rent prices, Corcoran said they’re going to continue to go up, and there won’t be any relief. When interest rates go up and chase people into the rental market, rents generally go up. But when interest rates go down, that doesn’t mean rent follows. Corcoran said she’s never met a landlord that brings down their rent, ever. And, most of us know how she feels about renting—that it’s a “no-win game.”

This story was originally featured on Fortune.com

Remember~ date the rate, marry the home. As the famous Will Rogers said ” Don’t wait to buy real estate, by real estate and wait. Good advice everyone and I am just the gal to help you so reach out with all your real esate questions and needs in the Puget Sound region.