Your Homegrown Real Estate Team Serving Home Buyers & Sellers In Snohomish County, North King County And Eastside Areas Of Our Great Puget Sound Region.

As the beauty of the Puget Sound region unfolds around us, it’s the perfect time to ensure your home remains a sanctuary of comfort and style. 🏡✨ Our team understands the unique needs of Puget Sound homes, and we’ve curated an essential annual maintenance checklist just for you. 🛠️🌲 From the roof overhead to the roots in the ground, let’s embark on a journey of home care that keeps your investment in prime condition. Your home deserves the very best, and we’re here to guide you through every step. 🌟 If you have any questions or need local service recommendations, don’t hesitate to reach out. Your Puget Sound home is a gem, and together, let’s ensure it continues to shine bright!

When retirement looms, financial stability is a gnawing concern for most people. Have I saved enough? What will inflation do to my nest egg? Will Social Security remain solvent? What are the health wildcards I haven’t planned for? As such, it’s wise to slash expenses and debt as much as possible, with the idea of entering retirement debt-free. For some, that means paying off the mortgage by accelerating their mortgage payoff.

Experian (https://bit.ly/3srAgU7) found that the average mortgage balance debt by generation in 2022 was: Generation X (age 42-57): $274,406| Baby Boomers (58-76): $189,155 | Silent Generation (77+): $139,999

If you’re able to afford to put extra cash toward your mortgage, doing an early payoff can be a powerful strategy that not only cuts interest payments but lightens the financial and emotional load during retirement, bringing peace of mind, more money for hobbies, vacations, and funds for healthcare and long-term care expenses.

Still, before deciding, you must take a complete look at your financial picture to be sure that a faster payoff is the best way to achieve your goals and to understand the potential sacrifices and downsides of such a move.

Here are nine considerations.

1. Understand the risks. If you have a relatively low mortgage rate, could you miss out on higher returns on your money by putting the extra toward your mortgage? Will you miss out on mortgage interest deductions? By devoting money to your mortgage, you’re lowering your liquidity. Will that lack of liquidity adversely affect your other long-term goals or short-term needs? For example, are you hoping to give a chunk of money to help a child with a down payment or planning to pay some of your grandchild’s college costs?

2. Examine your debts. If you have credit cards, personal loans, and other obligations, paying those off is better before accelerating your mortgage payments. First, pay off debts with higher interest rates than your current mortgage because consumer debt typically carries higher interest rates than mortgages.

3. Understand your mortgage agreement. Read your agreement’s fine print and talk to your lender to be sure there aren’t prepayment penalties and that you’re allowed to make extra payments.

4. Calculate your savings. How quickly do you want to pay off your mortgage? Can you afford to shave five years or ten years off your mortgage? Use an online mortgage calculator to see how much principal you must pay every month or year to pay off a loan in a certain number of years and how much you’ll save with an early payoff. The savings can be significant. According to a NerdWallet calculator (https://bit.ly/45MhzZR), for example, if you took out a $300,000 30-year fixed loan at 5.5%, have ten years left, and decide to pay it off in five years, you’d have to pay an extra $206.75 monthly. The move would save $89,796.84 over the life of the loan.

5. Develop your repayment plan. Will you make an annual lump-sum payment or extra payments monthly or bi-weekly? One advantage of spreading the additional payments across the year and making bi-weekly payments is that you lower your principal balance each month, creating a smaller balance on which interest is calculated.

6. Look at your budget. How much extra money can you afford to put toward your mortgage? Where can you cut back? Also, consider the sacrifices you’ll need to make and decide if missing out on a vacation or cutting back on hobbies is worth it.

7. Don’t sacrifice retirement savings. Have an adequate emergency fund before shifting money to speed up your mortgage payoff. Also, be sure you’ll still be able to max out all your retirement vehicles like 401ks, Roth IRAs, and Health Savings Accounts and make catch-up contributions.

8. Pay the right way. Be sure to tell your mortgage holder that your extra payments will be applied to the loan principal, not the next month’s mortgage payment.

9. Talk to experts. Remember that there’s no one-size-fits-all approach with finances, so get advice from financial pros—your accountant and financial planner, for example—to understand the risks and the impact an early mortgage payoff would have on your other goals.

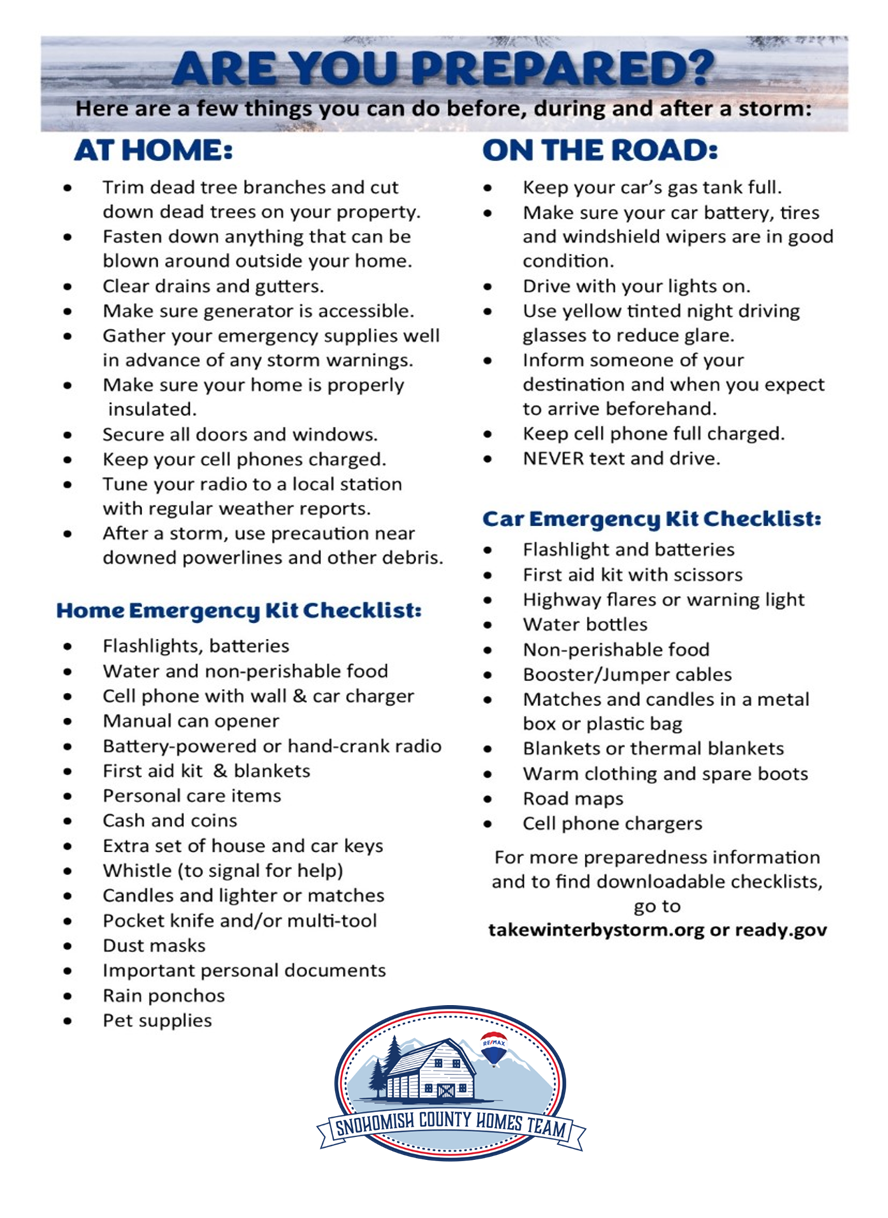

I know the last year has you asking yourself I don’t need to worry buyers are waiving inspections. I guarantee you that is changing and if you do not wish to have a Seller’s pre-inspection than you may wish to check out this list. You can make your home more attractive to buyers and increase your likelihood of obtaining a positive inspection report by performing routine maintenance now before going on the market.

A visual inspection does not pass or fail a house but simply describes those items in need of minor or major repair or replacement. The inspector will visually examine the structure, crawl space, attic, mechanical components and all interior rooms, as well as closets.

On the day of you can help by having keys available to any locked doors, removing obstacles around water heaters and other appliances, removing items from closets that provide access to attics, and so on. Please be ready to indicate the location of hidden components such as the water meter, electrical panel, sump pump and main sewer clean out.

You can eliminate seasonal limitations on the inspection by clearing pathways of snow or debris. Ensure that appliances not tested because of the temperature (such as air conditioners in winter) are operation. Move boxes and storage items away from interior walls and make certain the entire perimeter of the house can be observed. Finally, leave pets with a friend or, take them with you, for the few hours of the inspection.

EXTERIOR COMPONENTS

Repair minor defects in the exterior wall coverings.

Repair damaged masonry on walkways and steps.

Repair missing or loose railings on decks and steps.

Recaulk around exterior windows and doors.

Replace missing or damaged shingles

Recaulk around flashing.

Clean debris from gutters.

Ensure downspouts are intact and water drains away from the house.

Trim trees and shrubs away from the roof.

INTERIOR COMPONENTS

Loosen any windows that are painted shut.

Replace missing or faulty hardware on doors and windows.

Repair any broken or cracked windows.

Replace damaged baseboard or molding.

Recaulk around bathtub and kitchen/bathroom sinks.

Re-grout tub and shower enclosures and the kitchen backsplash.

Repair leaky faucets and fixtures.

Unclog slow drains using commercial cleaner.

Replace oversized fuses with proper fuses.

Repair faulty receptacles and switches.

Ensure exhaust fans are in working order.

Have the fireplace chimney swept.

Have the furnace or other major appliances serviced.

Ensure central vacuum, garbage disposal, water softener and other ancillary components not part of the standard inspection are in working order.

Replace dead batteries in smoke and CO detectors.

Have service contracts, manuals and warranties available and in a drawer for the inspector/buyer to access.

Prior planning always pays off and makes for a smooth transaction after securing a buyer. Reach out to me for questions on this or if you are considering selling your home.

It’s that time again for your monthly newsletter! Notice QR codes seem to be back? While I like QR codes and think they are handy I sure hope we all can “experience” some of the beautiful places the Pacific Northwest has to explore in person and soon!

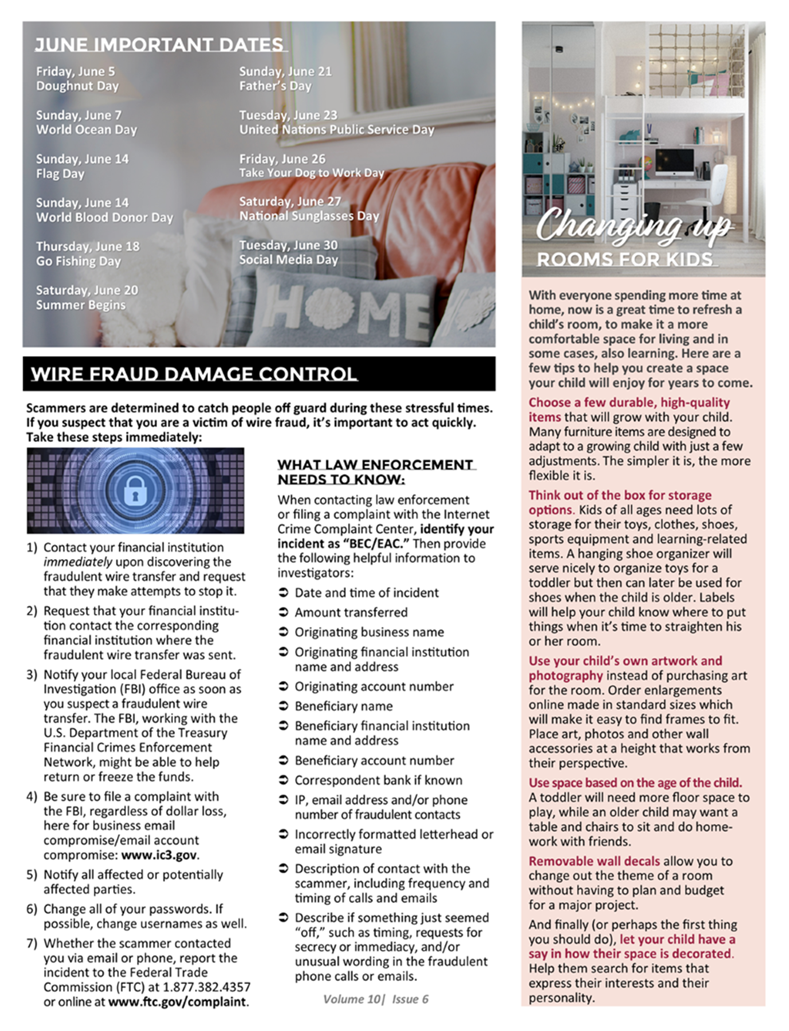

If you are refinancing, purchasing or selling this is a must read. I tell all my clients to call me first and double check if they get any suspicious email or phone call. Do not let this happen to you!